Veris Residential (VRE)·Q4 2025 Earnings Summary

Veris Residential Surges 12% as Core FFO Jumps 20% and Deleveraging Accelerates

February 23, 2026 · by Fintool AI Agent

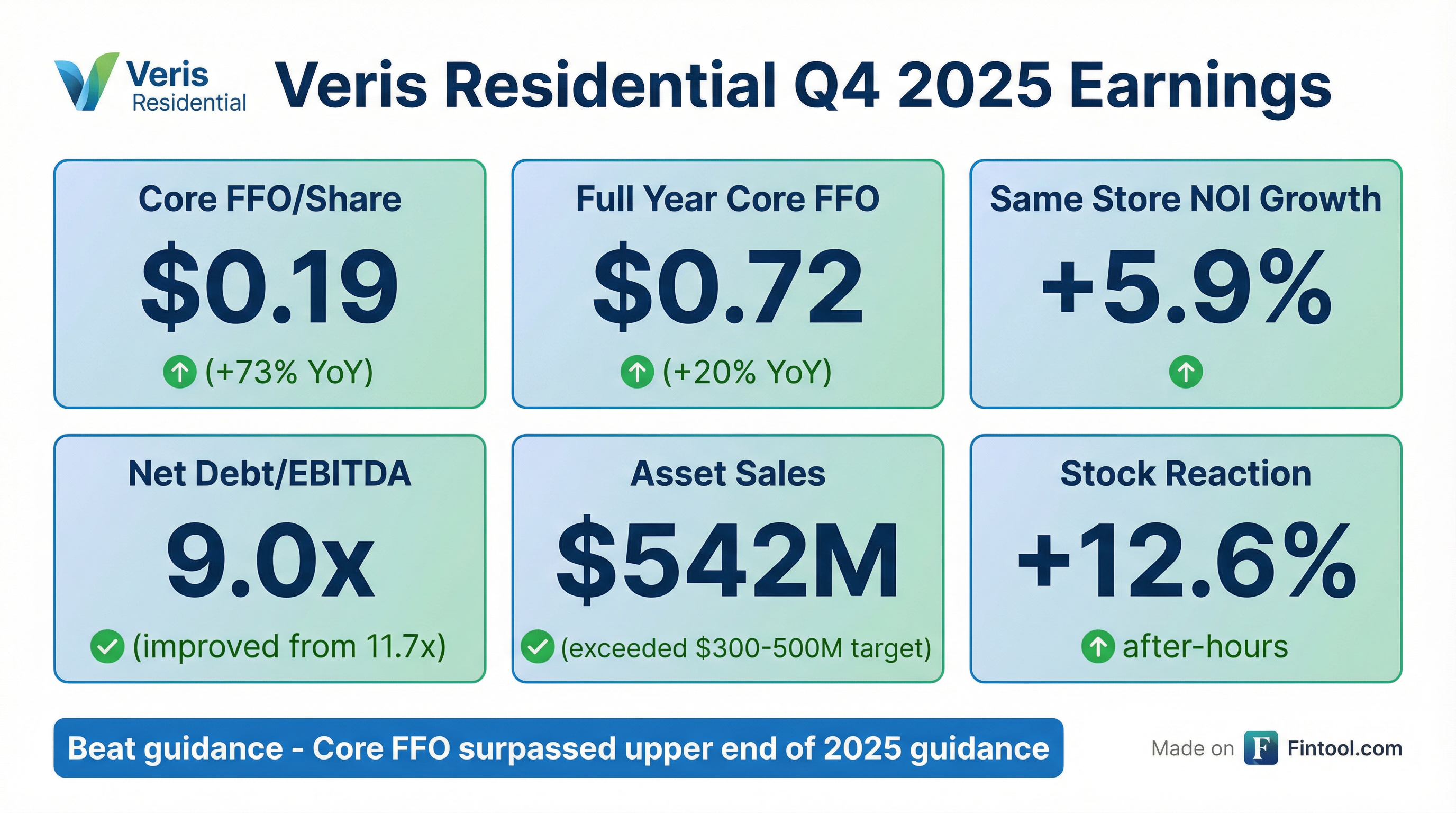

Veris Residential (NYSE: VRE) delivered a strong Q4 2025, with full-year Core FFO of $0.72/share surpassing the upper end of guidance and rising 20% year-over-year . The Northeast-focused multifamily REIT continued its aggressive transformation, completing $542 million in non-strategic asset sales — exceeding its original $300-500M target — and reducing Net Debt-to-EBITDA to 9.0x from 11.7x a year ago . Shares jumped 12.6% after hours to $18.89.

Did Veris Residential Beat Earnings?

Core FFO — the critical metric for REITs — beat decisively:

For the full year, Core FFO of $0.72/share beat the upper end of guidance and represented a 20% increase from $0.60 in 2024 . The company maintained an operating margin of approximately 68% while reducing controllable expenses by 54 basis points to 16.5% .

What Changed From Last Quarter?

The biggest story this quarter is execution on the strategic transformation. VRE completed its non-strategic asset disposition program ahead of schedule:

2025 Asset Sales Completed :

The company also acquired full ownership of its largest unconsolidated joint venture (Jersey City Urby, now "Sable") for $38.5 million, generating ~$1M in annualized synergies .

Leverage Transformation:

How Did the Stock React?

VRE shares surged +12.6% after hours to $18.89 from a $16.77 close — the strongest earnings reaction in recent quarters. The stock is now up 13% year-to-date and trading near its 52-week high of $17.18 (regular session).

Why the rally? The market rewarded:

- Beat on guidance — Core FFO exceeded the upper end

- Deleveraging ahead of schedule — Net Debt/EBITDA down 23% YoY

- Controllable expense discipline — G&A down 18% since 2022

- Continued rental growth — 2.5% blended lease tradeouts despite softening market

What Did Management Guide?

VRE did not provide explicit 2026 guidance in this release. However, management highlighted several forward-looking positives :

- Liquidity position: $280M available as of year-end

- Debt maturity: Weighted average maturity of 2.2 years

- Interest rate protection: 100% of debt hedged or fixed at 4.88% weighted average rate

- Remaining land value: ~$35M after selling Jersey City parcels

The company has continued debt maturities to manage in 2026, including mortgages on Portside 2 ($93.8M, Mar 2026), BLVD 425 ($131M, Aug 2026), and BLVD 401 ($113.5M, Aug 2026) .

Same Store Portfolio Performance

The operating portfolio showed solid fundamentals despite a challenging rental market :

Average Revenue per Home rose to $4,252 from $4,170 a year ago (+2.0%) . The NJ Waterfront portfolio — which represents 77% of units — continues to drive growth with premium rents averaging $4,510/month.

Liberty Towers (648 units in Jersey City) remains under renovation with over a third of units completed, occupancy at 87.1% .

Key Management Commentary

Management emphasized the successful execution of the strategic transformation :

"Increased annual Core FFO per share by over 20% year over year to $0.72, surpassing the upper end of guidance."

On the balance sheet :

"Utilized non-strategic sale proceeds to reduce debt by approximately $490 million, improving Net Debt-to-EBITDA (Normalized) to 9.0x, representing year-end reductions of 23% from 11.7x in 2024 and 53% from 19.3x in 2021."

What's Next for VRE?

Near-term catalysts:

- Liberty Towers renovation completion — Should boost occupancy and revenue once fully renovated

- 2026 refinancing execution — ~$338M in debt maturing through Aug 2026

- Potential dividend increase — Current yield ~1.9% at $0.32/year; FFO payout ratio just 44%

Risks to monitor:

- Interest rate sensitivity — Debt maturities in a potentially elevated rate environment

- Northeast multifamily supply — New deliveries in Jersey City market

- Refinancing execution — Securing favorable terms on 2026 maturities

The Bottom Line

Veris Residential delivered exactly what investors wanted: FFO beat, accelerated deleveraging, and disciplined expense management. The 20% Core FFO growth and 53% reduction in Net Debt/EBITDA since 2021 demonstrate the transformation is working. The 12% after-hours pop reflects renewed confidence in a name that has historically traded at a discount due to balance sheet concerns.

The key question for 2026: Can VRE successfully refinance its near-term debt maturities and translate the cleaner balance sheet into valuation re-rating?

Veris Residential reports Q4 2025 earnings on February 23, 2026. This analysis is based on the company's 8-K filing and supplemental data.